When you walk into an insurance office or sit down to renew your policy online, the terminology can feel like an entirely different language. In the fast-paced environment of the Delhi-NCR region, where FBD commuters are constantly balancing work and heavy traffic, nobody has the time to read through fifty pages of complex legal jargon. When locals search for gaadi ka insurance Faridabad, they usually ask for policies using highly colloquial terms—phrases passed down from mechanics, friends, and family.

We frequently hear FBD residents ask: “Bhaiya, isme bumper to bumper milega?” or “Mujhe sirf first party policy chahiye.” While these terms are deeply embedded in the local culture, they do not technically exist in official IRDAI (Insurance Regulatory and Development Authority of India) rulebooks. Understanding the direct translation of these local phrases into actual policy coverage is the only way to guarantee that your vehicle is truly protected when driving through crowded areas like Sector 15, Sector 16, or the bustling NIT markets.

In this comprehensive guide, Faridabad Insurance Wala decodes the exact differences between first-party, third-party, and the highly sought-after “bumper to bumper” insurance. By the end of this article, you will know exactly what you are paying for and how to shield your vehicle from the unpredictable realities of Haryana’s roads.

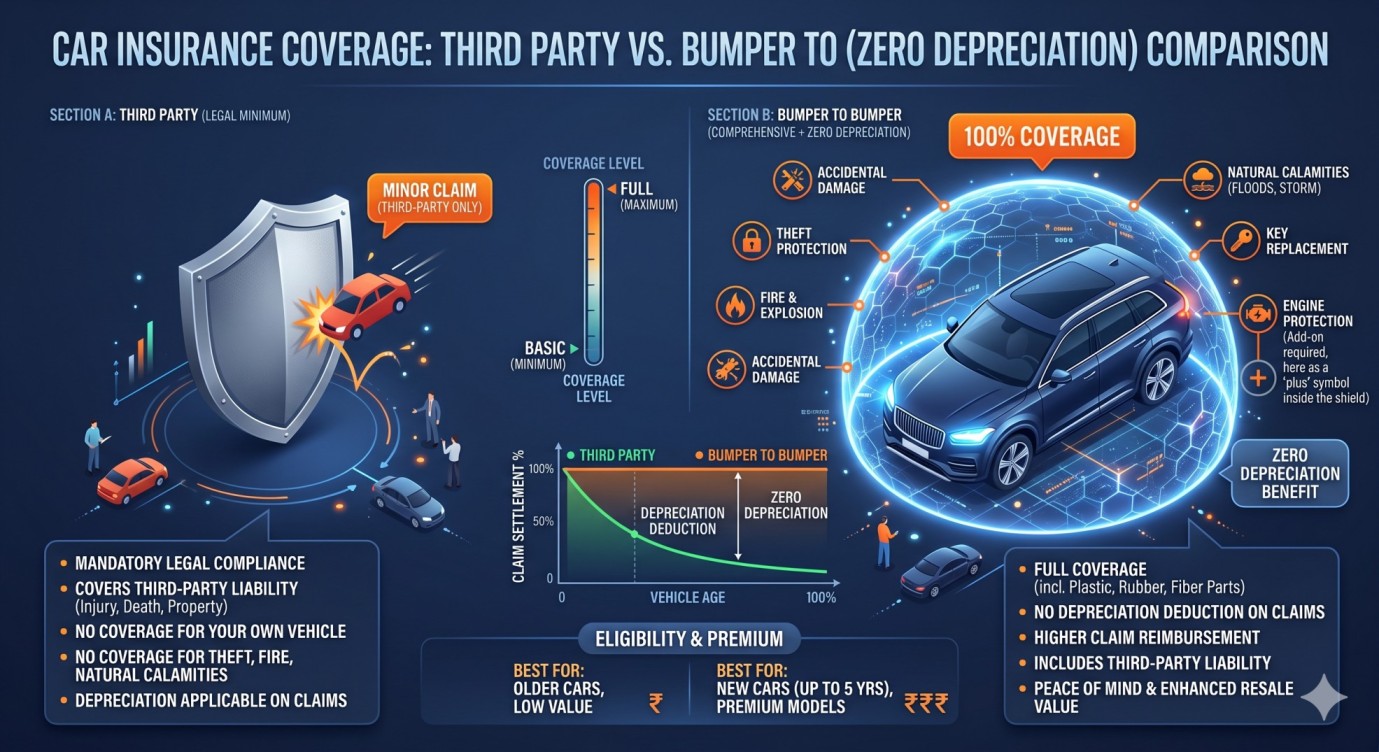

1. The Legal Baseline: What is Third Party Insurance?

If you have ever been stopped at a traffic barricade near Bata Chowk, the first document the traffic police demand is your insurance paper. What they are actually checking for is your third party insurance. Under the Indian Motor Vehicles Act, driving any vehicle on public roads without this basic layer of protection is a punishable offense leading to heavy challans.

Who is the “Third Party”?

To understand this, you need to know the three parties involved in an insurance contract:

- First Party: You, the owner of the vehicle.

- Second Party: The insurance company providing the policy.

- Third Party: Anyone else on the road—pedestrians, other drivers, passengers, or property owners.

Third-party insurance is strictly designed to protect the *other* person. If you accidentally rear-end a luxury sedan on Mathura Road, or if you accidentally damage a shop’s storefront in the local market, your third-party policy covers the legal and financial liabilities for their repairs and medical bills. The premium for this coverage is mandated and fixed by the government based on your vehicle’s engine capacity (CC).

The Hidden Danger: While a third-party policy keeps you legally compliant, it offers zero financial protection for your own car. If your vehicle is completely crushed in that same accident, or if it is stolen from outside your home, a third-party policy will not pay you a single rupee. Relying solely on this coverage is an incredibly high-risk gamble for private car owners.

2. Securing Your Asset: First Party Insurance (Comprehensive Cover)

When Faridabad residents ask for “first party insurance,” they are actually referring to a Comprehensive Motor Insurance Policy. This is the shield that protects your personal financial investment.

A comprehensive policy bundles the mandatory third-party liability cover with an “Own Damage” (OD) cover. This means that if your car is involved in a collision, the insurance company will pay for the repairs of the other person’s vehicle AND your vehicle.

What Does First Party (Comprehensive) Cover?

- Accidental Damage: Repairs required after a crash, whether it was your fault or the other driver’s.

- Theft: If your car is stolen from residential areas like Sector 15 or Sector 16, the insurer will pay you the Insured Declared Value (IDV) of the car.

- Natural Calamities: Damage caused by floods, earthquakes, cyclones, or falling trees during severe Haryana monsoons.

- Man-made Disasters: Financial protection against riots, strikes, vandalism, and malicious damage.

If you want absolute peace of mind and access to cashless garage networks, upgrading to a comprehensive policy through a trusted provider of car insurance faridabad is non-negotiable.

3. The Holy Grail: What “Bumper to Bumper” Insurance Really Means

Here is where the biggest confusion lies. Many car owners believe that buying a “First Party” (Comprehensive) policy means 100% of their repair bills will be paid by the insurer. Unfortunately, they are in for a rude shock at the garage billing desk.

In a standard comprehensive policy, insurance companies apply the rule of Depreciation. Over time, parts of your car lose their value due to wear and tear. When an accident happens, the insurer does not pay the full price for new replacement parts. Instead, they deduct a percentage based on the material of the part:

- Nylon, Rubber, and Plastic Parts (like bumpers): 50% deduction.

- Fiberglass Components: 30% deduction.

- Glass Parts: 0% deduction (fully covered).

If your front bumper is destroyed in a crash, a standard comprehensive policy will only pay 50% of the cost of the new bumper. You must pay the remaining 50% out of your own pocket. This is where bumper to bumper insurance comes into play.

The Zero Depreciation Add-on

In the official insurance world, “bumper to bumper” is known as a Zero Depreciation or “Nil Dep” add-on. When you attach this rider to your comprehensive policy, the insurance company waives the depreciation rules entirely. If your bumper is destroyed, the insurer pays 100% of the replacement cost (excluding a minor mandatory file charge/deductible). Because modern cars feature heavy use of plastic, fiber, and expensive sensors in their bumpers, this add-on saves you thousands of rupees during a claim.

4. Why FBD Locals Need Zero Depreciation More Than Ever

Driving conditions in the NCR are tough on vehicles. FBD locals face specific daily hazards that make the Bumper to Bumper add-on an absolute necessity for cars under 5 years of age:

- Heavy Two-Wheeler Traffic: The dense clusters in NIT and Ballabgarh are famous for unpredictable two-wheeler traffic. Scratches, broken side mirrors, and cracked plastic bumpers are weekly occurrences.

- Highway Debris: Commuting on the Mathura Road bypass often means dealing with flying stones and debris from heavy commercial trucks, which can easily shatter fiberglass components and expensive headlights.

- Tight Parking Spaces: In older sectors, tight parallel parking often leads to “hit and run” scratches while your car is stationary. A zero-depreciation cover ensures you aren’t financially penalized for someone else’s poor parking skills.

5. Why Choose Faridabad Insurance Wala for Your Policy?

Decoding these terms is only the first step. To ensure you actually get the coverage you are promised, you need an agent who acts with complete transparency. At Faridabad Insurance Wala, we don’t just blindly sell policies. We analyze the age of your car, your daily driving route, and your specific budget to recommend the perfect balance of first-party coverage and zero-depreciation riders.

We partner with top IRDAI-approved insurers to guarantee that when you ask for “bumper to bumper,” you are getting a watertight contract with a vast local network of cashless garages. Don’t leave your vehicle’s safety to chance or confusing online portals. Let local experts handle the fine print so you can drive tension-free.